How to Get Student Loans Out of Default: The Definitive Guide

Have you fallen into the student loan default pit? It’s okay. You may be experiencing a lot of feelings right now – discouragement, fear, shame, anger. That’s normal. Although student loan default seriously sucks, it’s not the end of your world. It’s important to remember that you can climb out of that pit.

There are three main options to get student loans out of default: repayment in full, consolidation, and student loan rehabilitation. Not making payments on your student loans was what got you into student loan default, so it makes sense that getting out of default requires some amount of money being paid towards your balance. The key difference between these options is how much money you pay upfront to get out of default.

The Three Paths out of Student Loan Default

Repayment in Full

The easiest way out of student loan default is to repay your student loans in full. Easiest, however, doesn’t mean it’s possible for everyone. In fact, this is probably one of the least commonly taken paths out of student loan default. Most borrowers don’t have enough money to pay off their entire student loan balance in one fell swoop. If they did, this probably wouldn’t be an issue.

If you’re thinking about taking on a personal loan to pay off your student debt in full, think again. This move could land you into even deeper debt, as personal loans tend to have higher interest rates than federal student loans.

Some people may be able to find ways to make repayment in full work for them. And the benefits of repayment in full are numerous. The best part of repayment in full? You’re instantly out of your student loan debt entirely.

Student Loan Consolidation

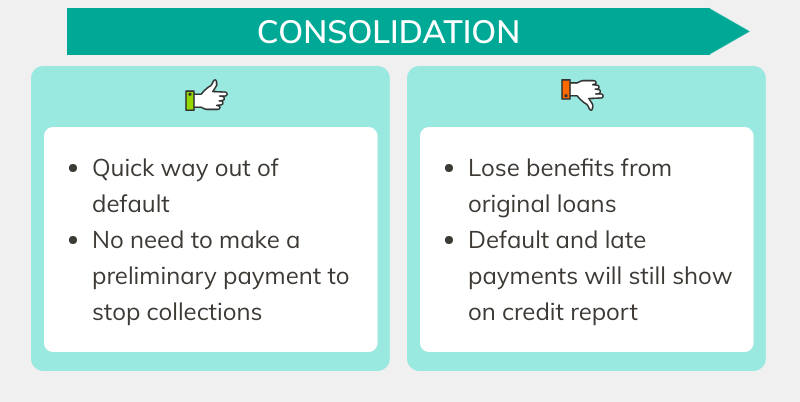

Consolidation is the next quickest way out of student loan default. This option consists of you paying off one or more of your federal student loans with a new federal consolidation loan. You can select your loan servicer once you consolidate. Consolidation will stop collectors from coming after you, so long as you keep making payments on your loans.

To qualify, you’ll need to either:

- Make three on-time, consecutive, full monthly payments on the defaulted loan, or

- Agree to repay your newly consolidated loan under an income-driven repayment plan.

If you choose to go with the first qualifying action, your servicer will determine the amount of those payments. But don’t worry – the amount will be based on your total financial circumstances.

If the second qualifying action is more your speed, you won’t need to make any preliminary payments to make your way out of student loan default.

If you choose to consolidate, there are a few drawbacks you should know about:

- The default and late payments will still show on your credit report for seven years.

- In consolidating your defaulted loans, you will lose any privileges and benefits specific to those loans.

- If you’ve defaulted on private student loans, consolidation won’t be an option for you, but student loan refinancing might be. You’ll need to talk with your servicer to see if refinancing is a possibility.

Student Loan Rehabilitation

Your third option is rehabilitating your loans. This process requires you contact your loan holder to begin the process. To successfully rehabilitate your federal direct or FFEL loans, you’ll need to:

- Agree in writing to make nine reasonable and affordable monthly payments within 20 days of the due date, and

- Make all nine payments during a period of 10 consecutive months.

The amount of those payments is determined by your loan holder. It is typically equal to 15 percent of your annual discretionary income, divided by 12. Your annual discretionary income is the amount of your adjusted gross income that exceeds 150 percent of the poverty guideline amount for your family size and state. So, if your annual discretionary income is $20,000, you’ll be looking at nine payments of $250.

If that amount is too high, you may still be able to negotiate a lower payment depending on your current financial situation.

Rehabilitation for Perkins loans is slightly different. Instead, you’ll need to make a full payment each month within 20 days of the due date for nine consecutive months to successfully rehabilitate federal Perkins loans.

Any wage garnishment will stop after your fifth rehabilitation payment. Once you’ve met the terms of your rehabilitation agreement, your student loans will no longer be in default and will return to good standing. You will then receive information about your new assigned servicer and where to send future payments.

While rehabilitation may take more time than consolidation, you will keep any benefits or privileges associated with your defaulted loans (like forbearance and deferment, student loan forgiveness, and repayment plan options).

When it comes to your credit report, rehabilitation is also slightly more attractive than consolidation. If you successfully rehabilitate your defaulted student loans, previously reported late payments will stay on your credit report but the notation of your default will be erased.

Which Path Should You Choose?

Each way out of student loan default has its strengths and weaknesses, as outlined above. Ultimately, only you can answer this question. If you’re having difficulty figuring out how to get your student loans out of default, one of our Student Loan Consultants can walk you through each option and how it could work in your life.

Avoid Another Fall into the Student Loan Default Pit

If being in student loan default felt bad, you definitely don’t want to experience it a second time. No one enjoys the threat of tax offset, wage garnishment, or collectors coming after you. Defaulting again also can have serious complications for the future.

If you rehabilitated or consolidated your student loans, you’ve just used your one “Get Out of Default Free” card. Should you fall back into student loan default, you will not have those options available to you again.

Here are some tips that should help steer you away from student loan default:

- Enroll in a repayment plan that works for you and your financial situation, like an income-based repayment plan.

- Set up automatic payments.

- Keep track of your loans.

- Record everything – monthly payments, your payment schedules, and information from any call you make to your student loan servicer.

If you ever fear you’re slipping back into delinquency or default, give us a call. We can help set you on the right track.

Disclaimer: The viewpoints and information expressed are that of the author(s) and do not necessarily reflect the opinions, viewpoints and official policies of any financial institution and/or government agency. All situations are unique and additional information can be obtained by contacting your loan servicer or a student loan professional.